You work hard for your money—so why does your paycheck vanish before the month does? It’s a familiar frustration. You get paid, the balance looks good for a few days, and suddenly you’re wondering where it all went. Rent, subscriptions, groceries, maybe a few delivery splurges—somehow it all adds up faster than you expect.

The truth is, most people leak money in small, mindless ways. Not because they’re careless, but because the modern money system is designed that way. Hidden fees, auto-renewals, missed benefits, high-interest traps—each one quietly drains your take-home pay before you even notice. Yet, most of these leaks are fixable without major lifestyle changes.

This article isn’t about cutting every joy or sprinting toward minimalism. It’s about using practical, slow-change habits that make your paycheck last longer and work harder for you over time. Think of it as a low-effort upgrade for your financial routine—small tweaks that quietly boost your take-home pay, simplify savings, and reduce money stress.

Ahead, we’ll break things down step by step—from understanding where your paycheck actually goes, to trimming silent costs, automating smart moves, and even making your employer’s benefits work in your favor. By the end, you’ll have a paycheck strategy that grows your financial breathing room—without adding another to-do list to your life.

Understand Where Your Paycheck Goes

Before you can maximize your paycheck, you first need to understand where it actually goes. It’s not as simple as subtracting monthly bills from what hits your account. There’s a hidden journey your money takes before it even lands in your hands.

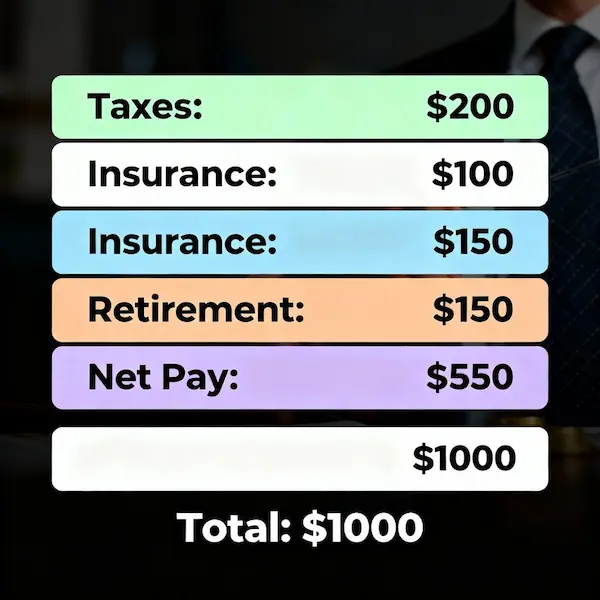

Your paycheck starts with gross pay—the total amount you earn before anything is deducted. Then comes take-home pay—the amount that finally reaches your bank account after taxes, insurance, and other contributions. That difference can be surprisingly large, and understanding why helps you take back some control.

Here’s what quietly chips away at your gross pay:

- Taxes: Federal, state, and sometimes local taxes automatically come out. Adjusting your tax withholdings slightly (through your W‑4 form, for example) can make a noticeable difference in how much you take home.

- Insurance premiums: Health, dental, and disability insurance premiums are often deducted right from your paycheck. These are essential, but knowing what’s taken—and whether you’re paying for coverage you don’t need—matters.

- Retirement contributions: Contributions to plans like a 401(k) or similar workplace account reduce your current take-home pay but help you invest for the future. The key is balancing near‑term cash flow with long‑term savings.

Most people never double-check their pay stubs. But small errors or unnoticed deductions can quietly cost you over time. Maybe your health plan changed but deductions didn’t, or a benefit enrollment didn’t process correctly. Taking five minutes each payday to review your stub can prevent those small mistakes from compounding across months.

Quick Tip: Spend 5 minutes after every payday tracking your paycheck flow—awareness is your first easy win.

Optimize Your Take-Home Pay

Maximizing your paycheck isn’t always about earning more—it’s often about keeping more of what you already make. One of the simplest ways to do that is by fine-tuning how much gets taken out before your money hits your account.

Start with your tax withholdings. Most people set their withholding preferences when they start a new job—and then never look at them again. But life changes, and so should your forms. If you consistently get large tax refunds every year, it means you’re over‑withholding. In other words, you’ve been giving the government an interest‑free loan. Log into your country’s tax portal or check with your HR team to review and update your W‑4 (or equivalent). Adjusting it to better match your actual tax liability can put extra cash into every paycheck without changing your income.

Next, take a smart look at your employer benefits. Many jobs offer pre‑tax options that reduce how much of your paycheck is taxable. Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs), and commuter benefits are powerful tools hiding in plain sight. Money you contribute to these accounts comes out before taxes are calculated, meaning you effectively save on every dollar you set aside. If your company offers wellness reimbursements or childcare support, those programs can also stretch your income further.

The goal isn’t to overcomplicate your financial life—it’s to make small, one‑time adjustments that quietly increase what lands in your account every pay period. These are the real money rules: small shifts in structure often beat big pushes for higher income. Because every extra dollar you keep today compounds into more freedom, less pressure, and stronger financial stability down the road.

When you’ve optimized your withholdings and pre‑tax benefits, your net pay becomes leaner, cleaner, and closer to its full potential. That’s the foundation for everything that comes next—automation, smarter spending, and meaningful growth.

Automate the Smart Stuff

Once you’ve optimized what you take home, the next step is to make that money move automatically in ways that work for you. The fewer choices you have to make every payday, the easier it becomes to stay consistent—and that’s how real financial progress happens.

Automation is the ultimate low-effort strategy. It removes the daily discipline battle and replaces willpower with systems. Start by setting up direct deposit splits. Most employers let you divide your paycheck into multiple accounts. Send a small percentage—say 10 percent—straight to your savings or emergency fund before the rest even lands in your checking account. When you never see that money, you never miss it. Over time, this quiet move builds a reliable cushion without any manual effort.

Next, let technology do the heavy lifting. Many modern banks and apps can automate savings in creative ways. Round‑up tools, such as those used by Acorns, Chime, or your bank’s built‑in features, automatically save your spare change from everyday purchases. Each transaction moves a few cents into savings without you having to think about it. These micro‑actions don’t feel big day to day, but they add up quickly across months.

You can also automate recurring transfers for bills, investments, or debt payments. This ensures you never miss deadlines, avoid late fees, and keep your credit profile strong—all while freeing up mental space. Consider pairing automatic transfers with regular, once‑a‑month check‑ins to make minor adjustments when needed.

The goal isn’t to build a complex system—it’s to design one that runs quietly in the background. Automation protects your progress from fatigue, forgetfulness, and temptation. By setting it up once, you create lifelong consistency that doesn’t depend on motivation.

Mini callout: One‑time setup. Lifetime consistency.

This is how you start letting your finances self‑manage, turning good money intentions into automatic results. It’s the easiest path from paycheck stress to steady growth—because smart systems always beat short bursts of discipline.

Cut the Silent Drains

Even the best paycheck strategy can leak if you don’t notice the small, steady drains quietly eating into it. These are the invisible expenses that slip under your radar—not because you’re careless, but because modern life makes it easy to forget them.

Start with subscriptions. Streaming services, apps, fitness memberships, or premium tools—many keep charging long after you’ve stopped using them. That five or ten dollars a month doesn’t seem like much until you multiply it by a year. Cancel just five unused $10 subscriptions and you’ve instantly reclaimed $50 a month, or about $600 a year. That’s a weekend getaway or a solid emergency fund boost, tucked back into your pocket.

Next, look at your recurring habits. Daily coffee runs, food delivery, or those “quick” store visits that always add one extra item—they add up faster than you think. None of these habits are bad in moderation, but they quietly nibble away at your financial margin. The key isn’t guilt—it’s awareness.

Technology can help. Apps like Mint, Rocket Money, or your bank’s spending insights automatically categorize transactions and flag recurring charges. They turn confusing statements into visual breakdowns so you can spot hidden costs in seconds. Set them up once and review them monthly. Unlike rigid budgets, these tools give you clarity without extra work.

You’re not being cheap; you’re taking control of invisible spending. That’s a huge mindset shift. Financial freedom often starts with reclaiming what you didn’t realize was slipping away. Once you plug those silent drains, every future paycheck feels a little lighter, a little freer.

The best part? This isn’t about endless micromanagement. It’s about effortless maintenance. When you identify and cancel what doesn’t serve you, the effects compound quietly in the background. You only need to do it once, and the savings repeat month after month—money that used to vanish now stays and builds.

By the time you’re done cutting the silent drains, you’ve transformed your paycheck from a leaky bucket into a purposeful flow—one that supports your goals instead of slipping through the cracks.

Make Your Employer Work for You

You might be surprised how much money your employer is already offering you—without you even noticing. Many workplace benefits quietly add value to your paycheck, yet most employees never take full advantage of them. The result? You could be missing out on hundreds or even thousands of dollars a year in “hidden raises.”

Start with the basics: your 401(k) match or pension contributions. If your company matches your retirement savings even partially, that’s free money. Every dollar you contribute up to the match limit instantly doubles its value. Think of it as a guaranteed return before you ever invest a cent in the market.

Next, explore non-retirement perks that increase your financial flexibility. Many organizations offer tuition reimbursement or professional development stipends that cover certifications, courses, or even seminars. Using them can upgrade your skills without touching your savings. Some employers also provide wellness programs, childcare support, or commuter reimbursements—all of which directly reduce your out-of-pocket costs.

Don’t overlook smaller, less‑advertised benefits either. Employee discount portals, company exclusive deals, or stock purchase programs can shave costs on everyday expenses or help you gradually build ownership in your company. Small perks stacked together turn into meaningful financial breathing room.

Ask HR Once—Earn More Forever

Most of these benefits require just one conversation or a quick form submission. Ask your HR department what’s available, sign up once, and watch the value play out with every future paycheck. The beauty here is consistency: even small contributions or discounts compound over time. You’re not taking on extra work—you’re activating benefits you’ve already earned.

By treating your employer benefits as part of your overall income strategy, you stretch the real value of every dollar you earn. One quick inquiry today can pay dividends for years.

Earn a Bit Extra Without More Work

Sometimes, the best way to grow your income isn’t by working harder—it’s by letting your money and habits quietly do some of the work for you. Boosting your paycheck power doesn’t always mean chasing a raise; it can also mean building small, passive streams that add to your bottom line with almost no extra effort.

Start with cashback tools. Many payment platforms and browser extensions turn your regular spending into quiet savings. Apps like Rakuten, Honey, or your credit card’s rewards program put small amounts of cash back into your pocket every time you shop or pay bills online. It’s not glamorous money, but it’s effortless—and it compounds over time. Think of it as getting a mini‑bonus every month simply by using smarter checkout tools.

Then there’s the clutter‑to‑cash route. Selling unused items through marketplaces like Facebook Marketplace, OfferUp, or eBay takes minimal time and clears space at the same time. A few small sales may not seem like much, but if you make this a once‑a‑month habit, it can add up to a few hundred dollars a year that would’ve just sat collecting dust.

To quietly grow what you already have, look into high‑yield savings accounts or micro‑investing apps like Acorns or Wealthfront. These tools automatically put your idle money to work, earning interest or investing spare change behind the scenes. You set them up once, and they quietly build momentum without needing your attention.

Automation ties it all together. Whether you’re earning cashback, selling unused items, or investing automatically, the formula stays the same: one‑time setup, lifetime results. The systems keep running—even when you’re busy doing other things.

Imagine your next “bonus” not coming from your boss, but from smarter everyday moves. With these small, steady habits, your financial life upgrades itself quietly—growing bit by bit without demanding more effort or hours.

Reinforce Long-Term Momentum

Once you’ve streamlined your paycheck and automated smart systems, your next goal isn’t to add more tasks—it’s to keep the rhythm going. Building financial momentum isn’t about perfection; it’s about continuing the small actions that already work for you. Momentum thrives on consistency, not intensity.

Set aside 10 to 15 minutes once a month for a quick paycheck review. Open your bank app, glance at your recent spending, and confirm your automated transfers are running as planned. This isn’t a deep budget meeting—it’s a light check‑in that keeps you aware and confident. One short session each month helps you spot issues early and remind yourself how far you’ve come.

Celebrate the small wins, too. If you saved an extra 50 dollars this month or canceled an unused subscription, that’s proof you’re building new money habits that stick. Treat those simple victories like habit loops—each success reinforces the next one. You’re not saving for the sake of deprivation; you’re building peace of mind through structure and progress.

The benefits extend far beyond your wallet. When you spend less time worrying about finances, you free up mental energy for creativity, relationships, and personal growth. The clarity that comes from financial stability isn’t just practical—it’s emotional. It lets you focus on what actually matters.

It’s not about doing more. It’s about doing once what will keep rewarding you long after the initial effort. Your paycheck no longer controls you—you control what it becomes. And over time, that steady confidence is what turns these money habits into lifelong financial freedom.

Quick Checklist – Your Minimal Effort Paycheck Plan

- Review your pay stub monthly to spot errors or unnoticed deductions.

- Adjust your tax withholding if you consistently receive large refunds or owe extra at tax time.

- Automate transfers to savings or debt payments right after every payday.

- Cancel dead subscriptions and remove unused recurring charges.

- Use your employer benefits—retirement match, reimbursement programs, and wellness perks all count as hidden income.

- Put small extra cash or cashback rewards into a high‑yield savings account to grow interest automatically.

- Revisit your system every few months to tweak and improve what’s already working.

When you treat every dollar like an employee, your paycheck starts working harder than you do.

Conclusion

Maximizing your paycheck isn’t about working longer hours or chasing extra hustles—it’s about applying small, lazy‑smart money rules that quietly stretch every dollar. The real financial wins happen when you stop trying to do everything at once and instead focus on small systems that work automatically. Over time, these low‑effort habits build real security, freedom, and calm.

Start this week by picking just one thing from the checklist and doing it today. Maybe it’s canceling an old subscription, setting up automatic savings, or reviewing your pay stub for the first time in months. Whatever it is, take that single step now and let it trigger momentum that keeps growing with each paycheck.

You don’t need more stress or structure—you need systems that run while you live your life. Minimal effort can unlock massive calm. Let your paycheck breathe—and so can you.