Remember that rush of opening your first bank account? You probably felt like you’d officially entered adulthood—standing in line with your ID and that first deposit slip, imagining all the possibilities. Maybe a bit of nervous excitement too. It felt like the start of financial freedom.

But here’s the twist most people don’t talk about: that same first account can quietly drain your money if you don’t understand how it really works. It’s not intentional—just tiny overlooked details. A $5 monthly fee here, an unnoticed overdraft there, a missed alert that turns into a bigger balance problem later. Those “small” mistakes add up faster than you think.

Your first bank account isn’t just a place to stash your cash; it’s your first real partnership with the financial system. The way you manage it sets patterns for how you’ll handle money long after you leave college or start your first job. And while everyone celebrates opening that shiny new debit card, few people talk about the fine print that quietly punishes beginners.

This article breaks down the most common mistakes people make with their first bank account—and how to avoid them before they cost you. We’ll tackle hidden fees, missed automations, security slip-ups, and the habit of using checking accounts like savings accounts. By the end, you’ll know exactly how to turn your first account from a passive money holder into a powerful financial tool.

Mistake #1 – Ignoring Account Fees and Minimum Balances

One of the sneakiest ways your first bank account can quietly drain your wallet is through the pile-up of small fees. They seem harmless at first—a few dollars here, a few more there—but taken together, they can easily cost you hundreds over a year.

Banks make money through more than just loans. That “free checking” account often comes with fine print that includes a monthly maintenance fee if your balance drops below a certain amount. Then there’s the overdraft fee, charged when you accidentally spend more than what’s in your account. Out-of-network ATM fees are another trap—paying $3 to $5 every time you withdraw cash outside your bank’s network. And if you happen to stop using your account for a few months, some banks add an “inactivity fee.”

It all adds up fast. Imagine Alex, a college student managing a part-time job and classes. They opened a basic checking account without reading the fine print, thinking it was free. A $10 monthly maintenance fee went unnoticed for six months, quietly eating away $60 for essentially nothing. Add a couple of out-of-network withdrawals, and that total crosses $75—all money lost because of avoidable account terms.

The fix is simple but powerful: choose a no-fee or low-fee account designed for your lifestyle. Many online banks, digital-first apps, or student accounts waive minimum balance requirements entirely. They also provide free access to broad ATM networks and better tools for managing your money on mobile. Before opening or keeping any account, check the bank’s fee schedule online or ask a rep directly what you’ll pay under normal use.

Your first account should help you build habits—not penalize you for learning. Start by choosing one that keeps more of your hard-earned money where it belongs: in your pocket.

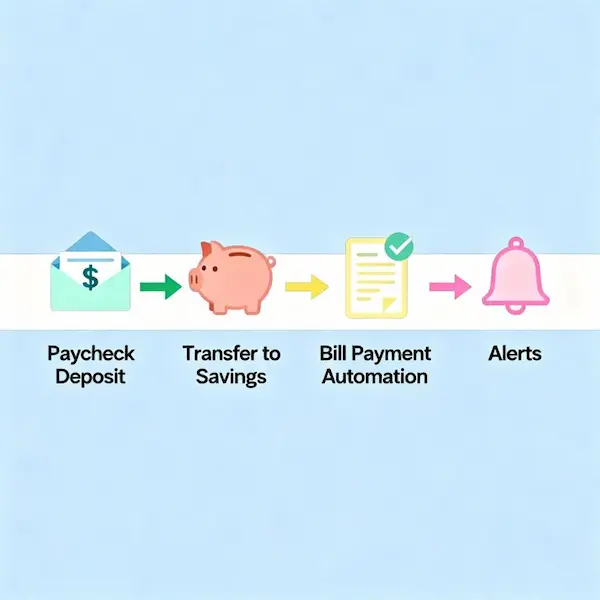

Mistake #2 – Not Setting Up Alerts or Automation

When you manage everything manually, it’s easy to miss something small that turns into something expensive. Maybe you forget your Spotify subscription is about to renew and your balance drops below $0, triggering an overdraft. Or you don’t notice that your direct deposit got delayed, and your rent payment bounces. These moments aren’t about irresponsibility—they’re signs that relying on memory for money management just doesn’t work in the long run.

Most banks and fintech apps offer powerful notification systems that take just a few minutes to set up. You can turn on mobile alerts for low balances, incoming deposits, and even unusual activity. A simple text or push notification can give you just enough time to move money, pause a payment, or adjust before a fee strikes.

Automation takes things a step further. You can schedule transfers every payday so a percentage of your income automatically moves to savings. The same goes for bills—setting them on autopay ensures nothing slips through the cracks. It’s less mental load, and more importantly, it keeps your financial rhythm consistent.

Here’s the mindset shift: automation builds consistency before discipline does. You don’t need to rely on willpower to save or pay on time when your systems do the heavy lifting for you. Over time, those small, automated decisions shape powerful financial habits.

Your goal isn’t to watch your account like a hawk—it’s to design a system that quietly protects your money while you live your life.

Mistake #3 – Using a Checking Account Like a Savings Account

If you keep all your money in one place, it’s almost impossible to know what’s safe to spend and what’s meant to be saved. That’s the biggest trap people fall into with their first bank account—treating their checking account like a savings account. When your spending cash and your future goals live in the same bucket, your mind naturally sees the total balance as “available,” even when part of it shouldn’t be touched.

Checking accounts are designed for movement—deposits, payments, transactions. They aren’t meant to hold money long-term. In most cases, they earn little to no interest, while high-yield savings accounts can pay several times more, helping your money quietly grow just by sitting there. More importantly, separating spending from saving builds awareness. You begin to see what’s actually available versus what’s meant to build stability.

A simple system works best: one for flow, one for growth. Use your checking account for bills, daily spending, and incoming paychecks—the “flow” of your money. Then, set up a linked high-yield savings account as your “growth” account. Move funds there automatically right after payday, even if it’s just 10 or 20 percent. Out of sight means out of temptation, and you’ll naturally spend less.

Picture Mia, who used to keep everything in one account. She’d open her app, see $1,200, and feel comfortable spending. But $400 of that was supposed to be her travel savings. By payday, that goal never grew. After splitting her accounts, she finally saw her savings start to climb—not because she earned more, but because she created structure.

The clearer your money system, the easier it becomes to stick with your goals—without feeling like you’re constantly fighting yourself.

Mistake #4 – Overlooking Security Basics

When most of your banking happens on a phone, it’s easy to forget that convenience always comes with risk. Many first-time account holders—especially digital-first users—assume that fraud or hacking happens only to “other people.” The truth is, online threats target the everyday habits we overlook, not the tech-savvy mistakes we imagine.

A few of the most common traps are surprisingly simple. Phishing emails disguised as bank alerts trick users into sharing login details. Weak or reused passwords open multiple doors if one account gets compromised. Logging into mobile banking from public Wi-Fi—like a café or airport—can expose private data to anyone on the same network. These aren’t rare risks; they happen to regular people every day.

The fix doesn’t require deep technical knowledge, just a few consistent habits.

- Use strong, unique passwords that combine letters, numbers, and symbols instead of easy phrases like names or birthdays.

- Turn on two-factor authentication (2FA), where your bank sends a verification code when you sign in.

- Avoid logging in or making transactions on public Wi-Fi. If necessary, use your phone’s data connection instead.

Unsafe habits can lead to frozen accounts, unauthorized transactions, and the headache of proving fraud before your funds are restored. Setting these protections now saves hours of stress and possibly hundreds of dollars later.

Think of digital banking security as locking your front door—you may not expect trouble, but it’s a simple step that protects what matters. Being proactive with online safety ensures that your first account remains secure, functional, and fully under your control.

Mistake #5 – Failing to Track Spending or Review Statements

It’s easier than ever to lose track of where your money goes. Between streaming platforms, food delivery apps, gym memberships, and cloud storage plans, today’s subscription culture runs mostly in the background. Payments renew automatically, and those small $5 or $10 charges barely register—until you check your balance and wonder where your cash disappeared.

This slow leak of money happens because many people never review their statements. When you’re busy, opening your banking app for more than a quick glance feels unnecessary. But that habit can hide problems: undetected subscriptions, duplicate fees, or even fraudulent charges. Banks do protect your funds, but only if you notice the issue and report it quickly. Ignoring your statements for months makes it harder to claim refunds or corrections later.

Picture this: that $8 fitness app you downloaded for a free trial months ago never got canceled. It’s quietly withdrawn $8 every 30 days, totaling nearly $100 by the end of the year—for something you don’t even use. Multiply that by a couple of forgotten subscriptions, and your “disappearing” savings suddenly make sense.

The easiest fix is to make tracking a weekly habit. Most banking apps now offer built-in analytics showing spending categories, trends, and upcoming bills. You can also export your transactions into a simple spreadsheet if you prefer hands-on review. Set aside ten minutes each week—like a Friday evening check-in—to scan for anything unusual.

Reviewing consistently isn’t about micromanaging every purchase; it’s about staying aware. When you catch small leaks early, you control your money instead of letting it quietly control you. The goal is simple: know exactly where each dollar goes and make sure it’s aligned with what matters to you.

Mistake #6 – Not Building a Relationship with Your Bank

Your bank might seem like a faceless app or website, but behind those systems are real people who can make your financial life much easier. Many first-time account holders overlook this human side, assuming it doesn’t matter as long as everything runs smoothly online. The truth is, building a simple relationship with your bank can open doors to better perks, faster support, and even future credit opportunities.

When you take a few minutes to connect—either by visiting a branch, using the chat support, or calling customer service—you often discover account options you didn’t know existed. Some banks quietly offer student-friendly accounts, automatic fee waivers, or cashback programs that aren’t heavily advertised. A quick conversation could save you real money or unlock tools that match your goals better.

Getting to know your banker also pays off later. When you’re ready to apply for a credit card, car loan, or even a mortgage, having an existing connection can help. A banker who recognizes you as a responsible customer is more likely to offer guidance, vouch for your history, or expedite approvals.

You don’t need to visit weekly—just being proactive once in a while builds goodwill. Relationships are currency in banking, too, and a simple conversation today might make tomorrow’s financial step a lot smoother.

Mistake #7 – Forgetting to Compare or Switch Accounts

Most people treat their first bank account like a lifelong relationship. It’s comfortable, familiar, and easy to keep. But convenience doesn’t always mean value. The financial world keeps evolving—banks introduce new policies, rates, and digital features—while your own financial needs shift as you grow. The account that was perfect when you were a student might quietly become expensive or limiting once you start earning more or managing larger balances.

It’s common to stay loyal simply because switching feels like a hassle. You already have your paycheck direct deposit set up and your bills auto-paid from that account. But here’s the truth: the extra fifteen minutes it takes to explore newer options could translate to hundreds of dollars saved each year in lower fees or higher interest returns.

There are a few key signs that it’s time to consider a switch.

- You’ve outgrown your student account and it’s started charging maintenance or activity fees.

- You’re earning more and want a higher annual percentage yield (APY) on your savings.

- You notice that digital-first banks or credit unions now offer perks your current bank doesn’t—cashback debit cards, real-time budgeting tools, or early direct deposits.

- You’re paying for basic banking services that others now offer for free.

Shopping for a better account isn’t about chasing every trendy app; it’s about finding a bank that grows with you. Look for transparent fee structures, strong mobile tools, and responsive customer support. Digital banks often lead in low or zero fees, while credit unions shine in personal service and better loan rates.

Your bank should evolve with your goals, not slow them down. Comparing options at least once a year helps ensure your money sits in the most beneficial place possible—working smarter, not just sitting still.

Bonus Tip – Smarter First-Time Money Moves

Once you’ve fixed the most common bank account mistakes, it’s time to go from simply managing money to making it work better for you. These quick, healthy habits can help you build financial momentum right from your first year of adulting.

- Link your checking and savings accounts for automatic transfers. Even a small recurring transfer—say, 10 or 20 dollars a week—adds up fast and ensures you’re saving without thinking about it.

- Round up purchases to the nearest dollar and send the spare change to savings. Many banks and apps can automate this, turning your daily spending into effortless micro-savings.

- Start a small emergency fund. Don’t wait to build the full three months’ worth—just focus on saving your first 300 to 500 dollars. That cushion protects you from overdrafts or those “oops” moments every beginner faces.

- Track your income versus spending each month. Use your banking app’s built-in analytics or a simple budget spreadsheet to understand where your money actually goes. Awareness is half the game.

- Celebrate small wins. That first month without fees, hitting your savings goal, or even catching an unnecessary charge early—all count. Positive reinforcement keeps you motivated to stay consistent.

Building smart money habits doesn’t require perfection, just small, steady actions. The goal isn’t to manage money like an expert—it’s to create systems so your money quietly works in your favor while you focus on life.

Wrap-Up

Your first bank account isn’t just a financial tool—it’s where your money story begins. The way you manage it now shapes how confidently you’ll handle larger financial moves later. Hidden fees, missed alerts, or blending spending with savings might seem like small oversights, but over time, they can quietly create stress and unnecessary loss. The good news is that every one of these mistakes is completely fixable once you start paying attention.

Small habits, like automating transfers, reviewing statements, and separating accounts for specific goals, build long-term stability. It’s not about perfection—it’s about progress. Each smart step you take today strengthens your financial foundation, helping you make clearer decisions and avoid common beginner pitfalls down the road.

Take a few minutes today to audit your own setup. Log into your account, explore your fee structure, check for old subscriptions, and set up any alerts you’ve been meaning to. You’ll be surprised at how empowering it feels to take control of something that once seemed complicated.

You’re not behind; you’re just getting smarter with every step. That’s what financial growth looks like—imperfect, intentional, and completely within your reach. Start where you are, use what you have, and keep refining as you go. Your first account isn’t just about banking—it’s about building confidence with every dollar you manage.